PEEK Interbody Devices Market: Forecast to 2034

PEEK (polyether ether ketone) interbody devices are implants used in spinal fusion surgery. Primary applications include lumbar (PLIF, TLIF), cervical, and thoracolumbar fusions. PEEK offers advantages over traditional metallic implants. Benefits include a modulus of elasticity close to natural bone, radiolucency for better imaging follow-up, biocompatibility, and reduced stress shielding. These implants support bone graft placement while maintaining spinal alignment. Raised incidence of degenerative disc disease, spinal stenosis, and herniated discs drives demand. Aging global populations face increased spinal disorders. Minimally invasive procedures using PEEK cages reduce recovery time and preserve tissue integrity.

OEMs increasingly offer surface-modified and hybrid PEEK devices with titanium- or hydroxyapatite-coated surfaces and porous architectures. Advances in 3D printing enable customized, patient-specific cage geometries. Regulatory approvals sustain rapid innovation in product lines.

Market factors include hospital infrastructure, reimbursement landscape, and surgeon preference. Regional variations emerge based on economic growth, healthcare investments, and local medical tourism trends.

The Evolution

Spinal fusion techniques date back decades. Metal cages made from titanium appeared in the late 20th century. Use of PEEK began in early 2000s. Implant properties matched surgeon and patient needs: radiolucent, elastic, inert. Initial PEEK cages were off-the-shelf designs.

Mid-2010s saw evolution toward porous and surface-treated designsadding osteoconductive coatings or titanium integration. Porous structures improved bone ongrowth and fusion rates. Additive manufacturing enabled customized cages based on patient CT scans.

Current generation devices integrate smart features such as radiopaque markers and expandable cage designs with lordotic geometry to match individual anatomy. OEMs such as Medtronic, Zimmer Biomet, Stryker, NuVasive, Alphatec, SeaSpine now offer next-gen PEEK systems for MIS (minimally invasive surgery).

Regulatory frameworks like FDA 510(k) and CE marking for medical devices validated novel designs and materials. Clinics and hospitals began adopting PEEK systems widely for complex cervical and lumbar cases.

Market Trends

Minimally invasive spinal procedures adopt PEEK cages widely due to reduced tissue trauma and recovery time benefits. 3D printing adoption accelerates customizing rigid PEEK geometries for unique patient anatomy. Surface modification trends focus on enhancing osseointegration using plasma or hydroxyapatite coatings.

Hybrid devices combining PEEK and titanium gain traction for mechanical strength plus imaging clarity. AI-driven surgical planning platforms integrate with PEEK systems to optimize sizing, alignment, and placement.

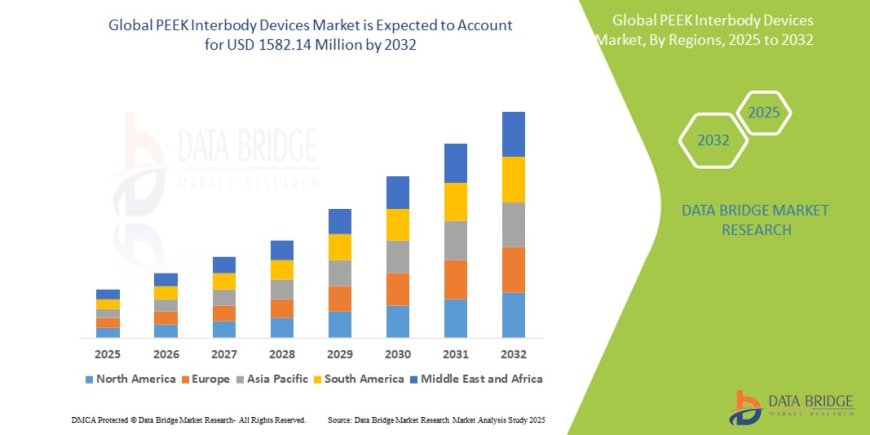

Regional expansion pushes innovation. Asia-Pacific sees highest growth with China forecast at 8.8% CAGR to 2030 and Chinas market valued at USD?640 million by 2030 Wikipedia+12GII+12Precedence Research+12OpenPR+1MarkWide Research+1Crystal Market Report+1Dataintelo+1. North America remains dominant with significant surgical volume and reimbursement and holds US$626 million market in 2024 GII. Hospitals control ~49% of usage while specialty clinics and ASCs claim ~30% and ~21% respectively . Posterior lumbar fusion is leading procedure for PEEK implants .

COVID-19 triggered more outpatient surgeries. Surgeons favor single-use PEEK devices to reduce infection risk. Market collaboration intensifies across OEMs and Tier 1 companies to improve device ecosystems.

Challenges

High cost of PEEK material and devices hold back adoption in budget-sensitive regions Reddit+12Crystal Market Report+12OpenPR+12. Regulatory approvals demand time and investment. PEEK file systems have to meet strict FDA/EMA guidelines Crystal Market Report. Alternatives like titanium and bioresorbables compete on performance and cost Dataintelo+11Crystal Market Report+11OpenPR+11.

Manufacturing complexities include precision machining, additive printing, and quality control. Certified facilities are required to meet ISO standards. Cost and learning curve challenges hamper mid-tier hospital adoption.

Lack of unified global standards for performance benchmarks complicates marketing across regions. Skepticism remains regarding long-term stability of surface modifications.

Uneven healthcare infrastructure limits growth in parts of Latin America, Africa, and rural Asia. Split reimbursement models restrict replacement rates.

Customization requires patient-specific imaging and design workflows. Surgeons need training and experience with advanced cage types.

Market Scope

Product Types

-

Lumbar interbody (ALIF, PLIF, TLIF)

-

Cervical interbody fusion devices

-

Thoracolumbar interbody (less common, niche)

Porosity & Surface Modifications

-

Porous and porous titanium overlays

-

Hydroxyapatite and plasma-sprayed coatings

-

Nano-texturing and bioactive surfaces

Form Factor

-

Static solid cages

-

Expandable cages

-

Anatomical lordotic designs

Applications

-

Degenerative disc disease

-

Herniated discs

-

Spinal stenosis, trauma, scoliosis, revision surgeries

Surgery Type

-

Open fusion

-

Minimally invasive procedures

End Users

-

Hospitals (~49% share)

-

Specialty spine clinics (~30%)

-

Ambulatory surgical centers (~21%) Precedence Research+4Future Market Report+4MarkWide Research+4Crystal Market Report+3MarkWide Research+3Professionals UK+3GIICrystal Market Report+10Future Market Insights+10Precedence Research+10GII+3GlobalData+3Professionals UK+3MarkWide Research+3Precedence Research+3Professionals UK+3

Regions

-

North America (largest share; US USD 626M)

-

Europe (strong due to reimbursement systems)

-

Asia-Pacific (fastest growing, China, India, Japan, S. Korea)

-

Latin America, MEA (emerging markets)

Distribution

-

OEM/wholesale to hospitals

-

ASC kit sales

-

Specialty clinic direct supply

Market Size and Forecast

Global market forecast: USD 2.6B in 2025, rising to USD 4.72B by 2033 (CAGR 7.74%) GII+1MarkWide Research+1Precedence Research+1Future Market Report+1. Another forecast values market at USD 5.0B by 2034 with 7.7% CAGR Professionals UK. Crystal Market Report projects USD 6.4B by 2032 at 7.6% CAGR Crystal Market Report. GlobalData estimates CAGR of 5.9% through 2033, outpacing overall spine fusion (~2.3%) GlobalData.

Product Segments

Posterior lumbar fusion holds largest share due to volume and radiolucency advantage, enhanced by MIS technique rise Crystal Market Report+7DataM Intelligence+7GII+7. Cervical cages capture growing share with ACDF procedures.

End Users

Hospitals are dominant. ASCs grow faster due to outpatient reimbursement. Specialty clinics continue expanding.

Regional Highlights

North America remains largest due to medical adoption and population demographics Dataintelo+4MarkWide Research+4Reddit+4Professionals UK+2Future Market Report+2Precedence Research+2GII. Asia-Pacific fastest-growing, driven by medical tourism and urbanization GII+1MarkWide Research+1. China projected at $640M by 2030 GII.

Drivers

-

Aging population with spinal disorders

-

Preference for PEEK properties (elasticity, imaging clarity)

-

Minimally invasive surgery trends

-

Surface modifications improving outcomes

-

3D printing enabling customizable cages

-

Medical tourism in APAC

Restraints

-

High material and procedure costs

-

Regulatory barriers

-

Alternative materials

-

Complex manufacturing needs

Factors Driving Growth

Aging population leads to rising spinal degeneration and fusion needs. POP aged over 50 drives higher uptake Wikipedia+7Professionals UK+7Crystal Market Report+7MarkWide Research+10GlobalData+10arXiv+10. Radiolucency allows superior post-op monitoring, especially critical in PLIF and TLIF procedures Wikipedia+4DataM Intelligence+4Future Market Report+4. Technological innovations provide better clinical results and surgeon confidence. MIS fuel adoption due to shorter recovery. Market expansion into ASCs and specialist clinics expands access. Healthcare infrastructure improvements in Asia-Pacific support growth. OEM launches and product innovation (coatings, 3D-printed formats) support premium pricing. Government healthcare support and rising expenditure drive new device uptake. Medical tourism brings cost-effective surgery demand for PEEK implants.

Source: https://www.databridgemarketresearch.com/reports/global-peek-interbody-devices-market

Conclusion

PEEK interbody devices represent a dynamic, growing segment in spinal implants. Market valued at USD 2.6B in 2025, expanding to USD 4.76.4B by 20302034, CAGR between 5.97.8%. Growth fueled by demographics, technological innovation, procedural shifts, and regional development.

Design improvements such as porous structures, surface coatings, and expandable features improve clinical adoption. Minimally invasive techniques and cost-effective outpatient care will further penetration. Asia-Pacific represents the fastest-growing region; North America remains leader. Challenges include material cost, regulatory burden, manufacturing complexity, and competition from titanium and bioresorbable implants. Collaboration on standardization, surgeon education, and cost optimization will help overcome barriers.

Future success requires R&D for performance and affordability, partnerships with surgeons and clinics, and regulatory harmonization. Continued innovation will solidify PEEK devices as dominant spinal fusion materials offering optimal fusion rates, patient outcomes, and imaging clarity.

Tags: PEEK interbody devices, spinal fusion implants, porous PEEK, interbody cages, minimally invasive spine surgery, orthopedic biomaterials, spinal implant market, Asia-Pacific medical device growth, 3D-printed implants, spinal health innovation